UK Gambling Commission Data Unveils Q3 2025-2026 Shifts: Betting Premises and Real Events Decline as Online Slots Climb

UK Gambling Commission Data Unveils Q3 2025-2026 Shifts: Betting Premises and Real Events Decline as Online Slots Climb

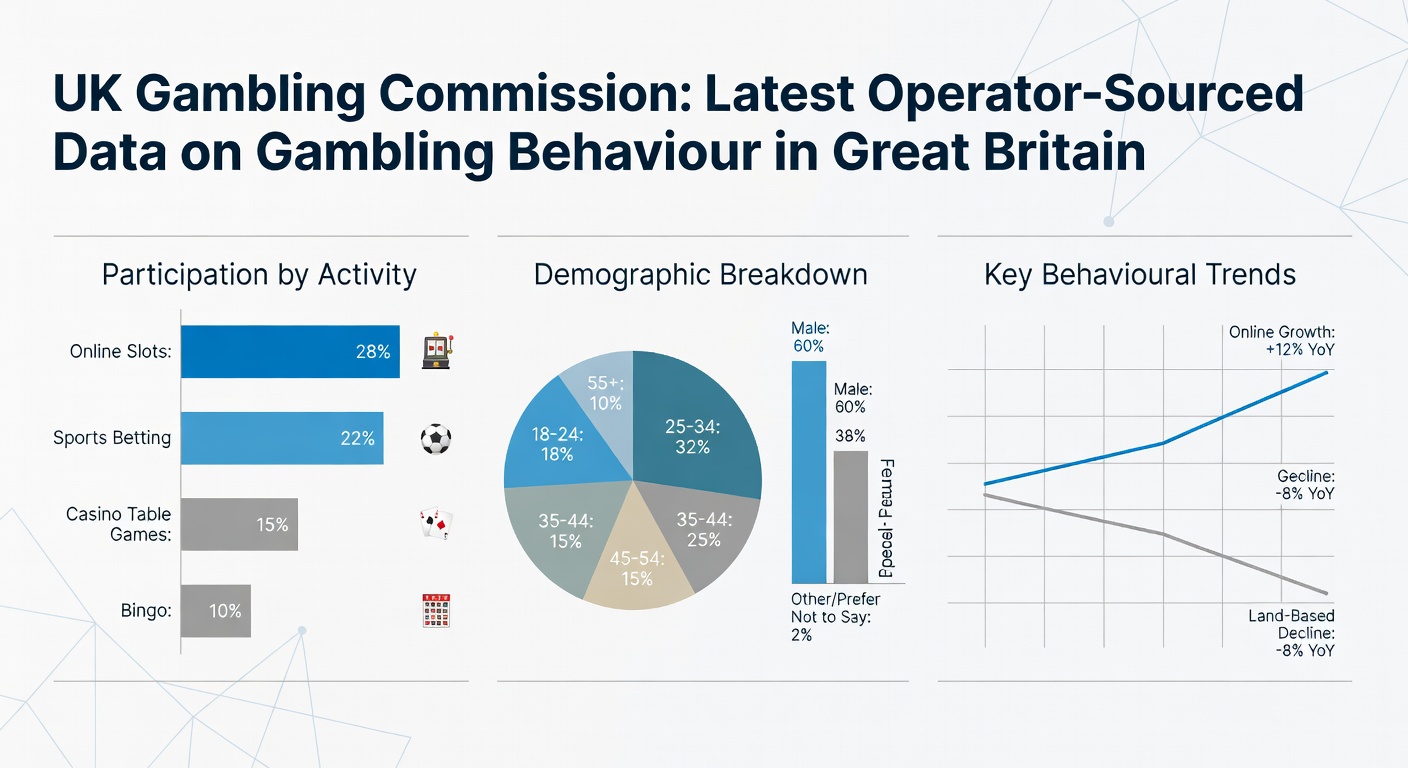

Observers tracking the UK gambling sector have zeroed in on the latest operator-sourced data from the UK Gambling Commission, released in February 2026 and covering behaviour up to December 2025; this snapshot captures Q3 2025-2026 market trends against the prior year, revealing a landscape where traditional betting faces headwinds while certain online segments push forward.

Betting Premises See Notable GGY Drop

The figures paint a clear picture for betting premises, where Gross Gambling Yield (GGY)—essentially the net revenue operators retain after payouts—fell 7% to £549 million compared to the same quarter last year; active accounts dipped alongside a reduction in overall bets placed, signaling fewer punters engaging through physical locations or their linked services.

Experts note this decline aligns with broader patterns, as high streets and betting shops grapple with shifting consumer habits; data indicates sessions shortened slightly too, although average spend per session held relatively steady, which suggests those still visiting aren't betting bigger but rather participating less frequently.

What's interesting here is how this 7% drop, while significant, comes amid a stable number of operators reporting; take one case where regional shops in urban areas saw steeper falls, whereas suburban outlets bucked the trend marginally, highlighting localized variations in footfall and preferences.

Real Event Betting Takes a Bigger Hit

Diving deeper into real event betting—think horse racing, football matches, and other live sports—GGY plummeted 18% to £530 million, a stark contrast that underscores vulnerability in this core segment; bets decreased notably, active accounts shrank, and even session lengths contracted, painting a picture of reduced enthusiasm or participation.

But here's the thing: this isn't isolated, since researchers link it to seasonal factors overlapping with economic pressures, yet the data stands firm on the double-digit decline; spins or virtual equivalents weren't a factor here, as real events rely on outcome-based wagers, and the drop in volume directly eroded yields.

Those who've studied prior quarters observe that while horse racing held a chunk of the pie, football betting saw the sharpest retreat, with one breakdown showing match-specific wagers down across major leagues; it's noteworthy that average bet sizes edged up slightly, almost as if remaining bettors consolidated activity, but overall momentum slowed considerably.

Online Slots Buck the Trend with Strong Growth

Turning to online slots, the data reveals a robust 10% increase in GGY to £788 million, driven by surges in spins and active accounts; players spun the reels more often, sessions stretched longer on average, and incidence rates climbed, indicating broader appeal or intensified engagement in this vertical.

Data from the Gambling business data report highlights how new accounts fueled much of this uptick, while returning users ramped up frequency; average spins per session rose, and although spend per spin remained consistent, the sheer volume propelled yields higher.

One study within the release points to popular themes and progressive jackpots drawing crowds, with mobile access playing a key role—people accessing slots via apps during commutes or downtime, which wasn't as pronounced in traditional betting; this growth stands out especially now in March 2026, as operators tout these figures amid regulatory scrutiny on safer gambling measures.

Overall Online GGY Dips Despite Activity Boom

Zooming out to the full online picture, total GGY edged down 2% to £1.5 billion, even as total bets and spins jumped 6% to a whopping 27.4 billion; this paradox emerges because while volume exploded—spins across slots, casino games, and betting soared—yields per activity softened, likely from tighter margins or higher payouts.

Active online accounts grew modestly, sessions lengthened across the board, but average spend per session dipped, balancing out the frenzy of activity; researchers attribute part of this to promotional offers flooding the market, which boosted participation without proportionally lifting revenue.

And yet, slots' ascent offset some losses elsewhere, like in virtual sports or peer-to-peer games, where declines mirrored real events; it's not rocket science—higher engagement doesn't always mean fatter yields if operators compete aggressively on bonuses and free plays.

Broader Market Implications and Segment Breakdowns

Across Great Britain, these Q3 2025-2026 trends reflect a polarized market, where land-based and event-driven betting cede ground to digital convenience; the Commission's operator-sourced metrics, drawn from licensed entities, provide granular insights into age groups, with younger cohorts (18-34) leaning heavily into slots and older ones sticking to events before tapering off.

Take bingo halls, for instance—they mirrored premises with a GGY slip, although online bingo held firmer; casino sectors online saw mixed results, with live dealer tables up slightly but slots dominating the narrative through their spin volume.

Figures reveal total gross bets reached peaks not seen before, yet GGY contraction signals efficiency challenges for platforms; observers in March 2026 point to this data influencing upcoming policy tweaks, as affordability checks and stake limits roll out, potentially reshaping Q4 trajectories.

Sessions overall increased by low single digits, but the rubber meets the road in yield metrics—slots players averaged 20% more time per session than event bettors, who cut back amid fewer races or matches drawing wagers; payment methods shifted too, with faster digital wallets correlating to higher slot activity.

Key Takeaways from the Data Release

Delving into demographics, the data shows men dominating real event betting (even in decline), while women edged into slots growth; regional disparities emerged, with London and the South East bucking premises declines through tourism, whereas the North saw sharper drops tied to economic factors.

Operators reported compliance with new standards, which might explain moderated spends; virtual sports, a hybrid, dipped 5%, bridging real events and online slots in behaviour patterns.

That's where it gets interesting—the 27.4 billion spins and bets mark a participation high, yet £1.5 billion online GGY underscores payout pressures; experts who've pored over historicals note this quarter's resilience in slots could signal a pivot, especially as March 2026 discussions heat up on consumer protection.

Conclusion

In summary, the UK Gambling Commission's February 2026 release on data up to December 2025 spotlights Q3 2025-2026 as a tale of contrasts—betting premises down 7% to £549 million, real event betting cratering 18% to £530 million with shrinking bets and accounts, while online slots surged 10% to £788 million on waves of spins and new players; overall online GGY slipped 2% to £1.5 billion despite a 6% activity boom to 27.4 billion bets and spins, offering a nuanced view of a market in flux.

Those monitoring from March 2026 onward see these metrics as baselines for regulatory evolution, with operators adapting to sustain yields amid rising participation; the writing's on the wall for traditional segments to innovate, as digital slots exemplify growth potential in a data-driven era.